At DreamWork Financial Group, we believe that understanding financial jargon is an important step in making better investing decisions. When you understand these terms, you can discover new strategies and feel confident discussing them with an advisor. That’s why we define useful, but commonly overlooked, financial strategies – like tax loss harvesting.

While the term “tax loss harvesting” sounds complicated, it isn’t. This strategy is simple to understand and, when implemented for the appropriate situation by an experienced wealth manager, it can reduce your capital gains and ordinary income taxes.

Capital Gains Tax – The Reason Behind Tax Loss Harvesting

Before defining tax loss harvesting, it makes sense to begin with a definition of capital gains tax – the main reason tax loss harvesting exists. Capital gains tax is a tax on the profits from selling an asset. Since stocks are considered assets, when you sell one for more than you paid for it, you will likely owe capital gains tax.

The amount of tax you owe on investment gains depends in part on how long you held the asset. When you sell an investment held less than one year, you incur a short-term capital gain. These are taxed at ordinary income tax rates. Conversely, if you sell an investment held longer than one year, you incur a long-term capital gain. These are taxed at a reduced rate for most investors.

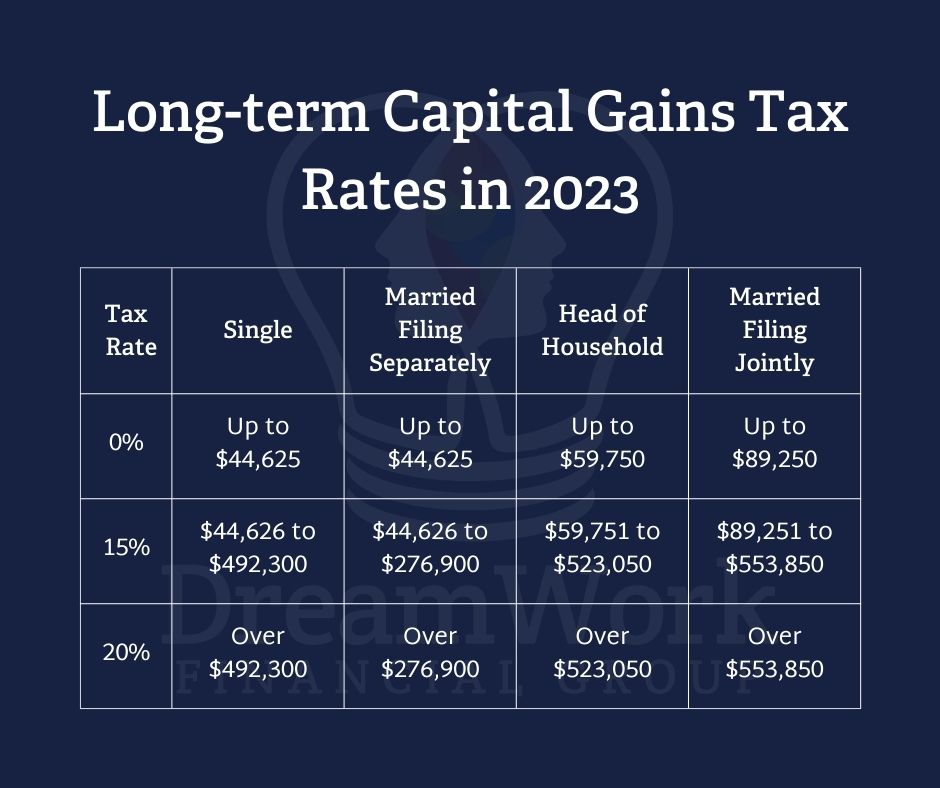

Long-term capital gains tax rates are based on your income and filing status. The rates pictured below apply to most investments, but some less-common assets – like qualified small business stock and collectibles – are taxed at different rates.

Tax Loss Harvesting Can Reduce Capital Gains and Income Taxes

Because tax is owed on net capital gains for the year, investment losses offset gains to reduce tax liability. Tax loss harvesting is an investing strategy that involves deliberately incurring capital losses to offset capital gains for tax purposes.

With tax loss harvesting, you elect to sell shares that are valued below your purchase price and use those losses to offset other gains – therefore reducing your net tax burden. However, it is important to remember that all investing decisions should be made with your goals in mind – so never sell investments solely for tax purposes. Tax loss harvesting isn’t a method for determining which stocks to eliminate from your portfolio, but rather which shares to sell once you have already decided to reduce exposure to a particular sector or company.

In addition to reducing capital gains tax, tax loss harvesting can also help reduce ordinary income tax up to $3,000 per year ($1,500 for married filing separately). If your net losses exceed $3,000 you may be able to carry the loss forward to subsequent years.

Tax Loss Harvesting in Practice

To illustrate the concept of tax loss harvesting, consider this simplified example:

While reallocating your portfolio, you and your advisor decide to eliminate Investment A and reduce holdings of Investment B. You realized a $10,000 gain from the sale of Investment A, so your advisor recommends using tax loss harvesting to sell shares from Investment B that are trading at a loss. In doing so, you realize a $15,000 loss from Investment B.

Because you recognized such a significant loss from Investment B, you offset gains from Investment A, eliminating capital gains tax on those profits. Additionally, you reduce your taxable income by $3,000, and carry forward a $2,000 loss. At a 35% tax rate, you save $4,550 in taxes this year and carry forward a $2,000 loss to use in subsequent years.

Tax Loss Harvesting in Conjunction with Other Investing Strategies

Most people invest to generate profits, not losses. But you may have losses from certain companies or tax lots, even if your overall portfolio performance is positive. Two investing methods can help you effectively tax loss harvest without compromising overall portfolio gains. These are direct indexing and dollar cost averaging.

Direct Indexing and Tax Loss Harvesting

Direct indexing involves purchasing the underlying securities in an index rather than a mutual fund or ETF. With this investing method, you own dozens or hundreds of stocks, rather than a few mutual funds.

While tax loss harvesting is possible with mutual funds, it is easier when you have more investments to choose from. For example, if you own a few sector-specific mutual funds and want to reduce holdings in the tech sector, your only option is to sell shares of the tech mutual fund, no matter if that fund is trading at a profit or a loss. On the other hand, if you own the underlying securities, you can choose to sell specific companies. This can be beneficial for eliminating poor performers from your portfolio and generating losses for tax loss harvesting.

Dollar Cost Averaging and Tax Loss Harvesting

Dollar cost averaging involves buying a fixed amount of a security on a regular basis regardless of share price. This creates dozens of tax lots – a record of each purchase for use in determining tax consequences. When you want to sell a stock, you can choose to sell the lots that have performed the worst to generate losses.

Dollar cost averaging can help you tax loss harvest, even with mutual funds and ETFs, but it is especially effective when used in conjunction with direct indexing. That’s why it’s important to find a wealth manager with the experience to build a custom portfolio, help you with dollar cost averaging, and choose the most advantageous lots to sell when rebalancing. When all these strategies are used together, you can manage taxes and maximize returns.

Tax Loss Harvesting with Investing Gameplan™ By DreamWork Financial Group

Investing Gameplan™ by DreamWork Financial Group is a unique wealth management program that allows investors to access custom portfolios and fiduciary advice. With Investing Gameplan™, you get a personalized portfolio and access to a wide range of investing strategies – like tax loss harvesting, dollar cost averaging, and direct indexing.

In the past, personalized wealth management was reserved for the very wealthy. But there are no minimum account balances to participate in Investing Gameplan™ – so just about anyone can easily get started. With Investing Gameplan™ by DreamWork, You Don’t Have to Be Wealthy to Have Wealth Management®.

Contact us today to get started.